Emissions reporting will soon be table stakes for any organization that wishes to stay ahead of the pack on environmental impact, attract an ever-growing group of environment-first consumers, or even secure funding and investment.

There are myriad methods for measuring and reporting organizational and product impact, some of which include Carbon Footprinting, Life Cycle Assessment (LCA), among more general and less common environmental risk assessments.

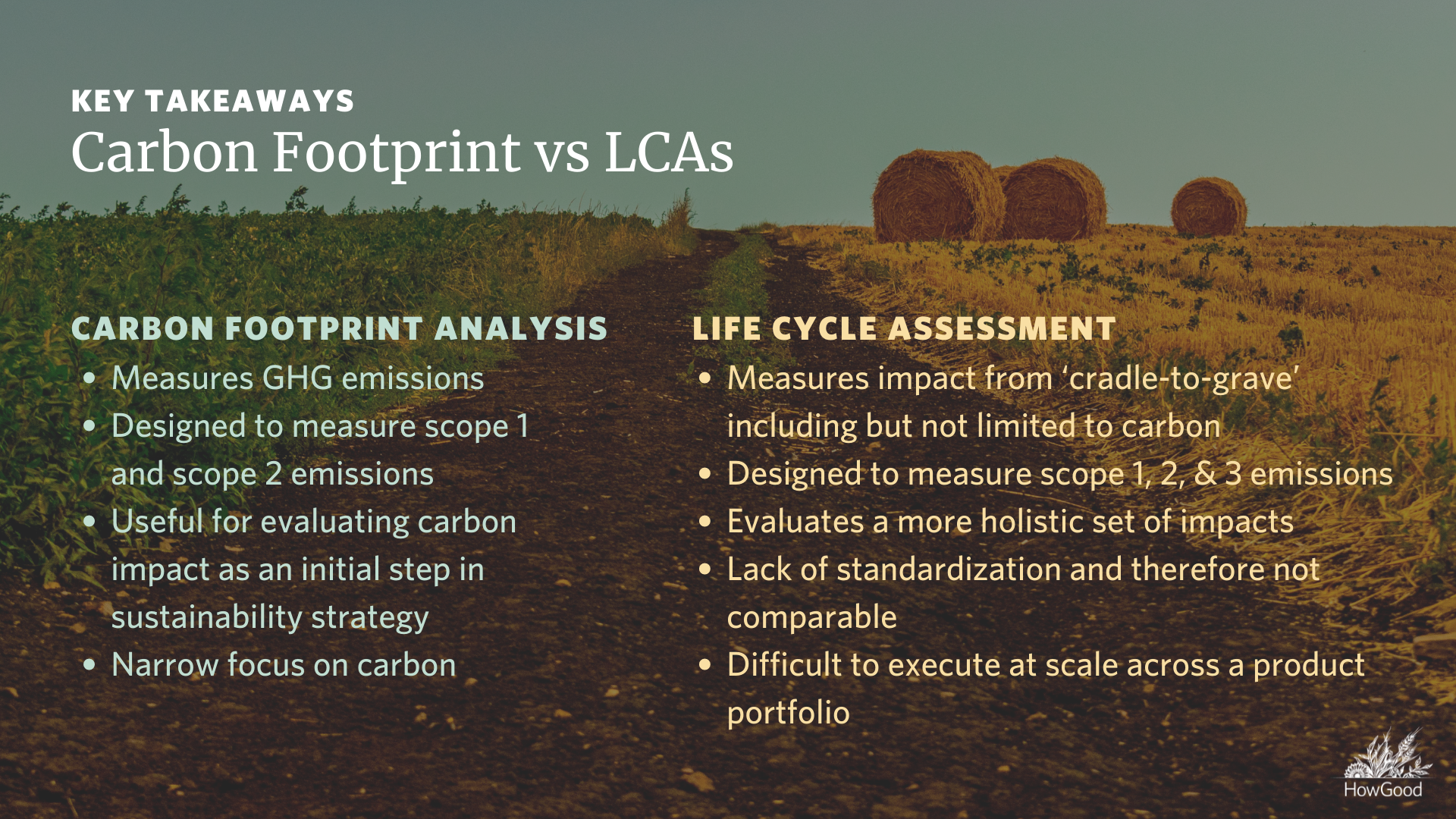

Carbon Footprint Analysis and LCAs were developed for a similar impetus–to measure the impacts companies have on planetary and environmental health–but their purposes were quite different.

History of Carbon Footprints

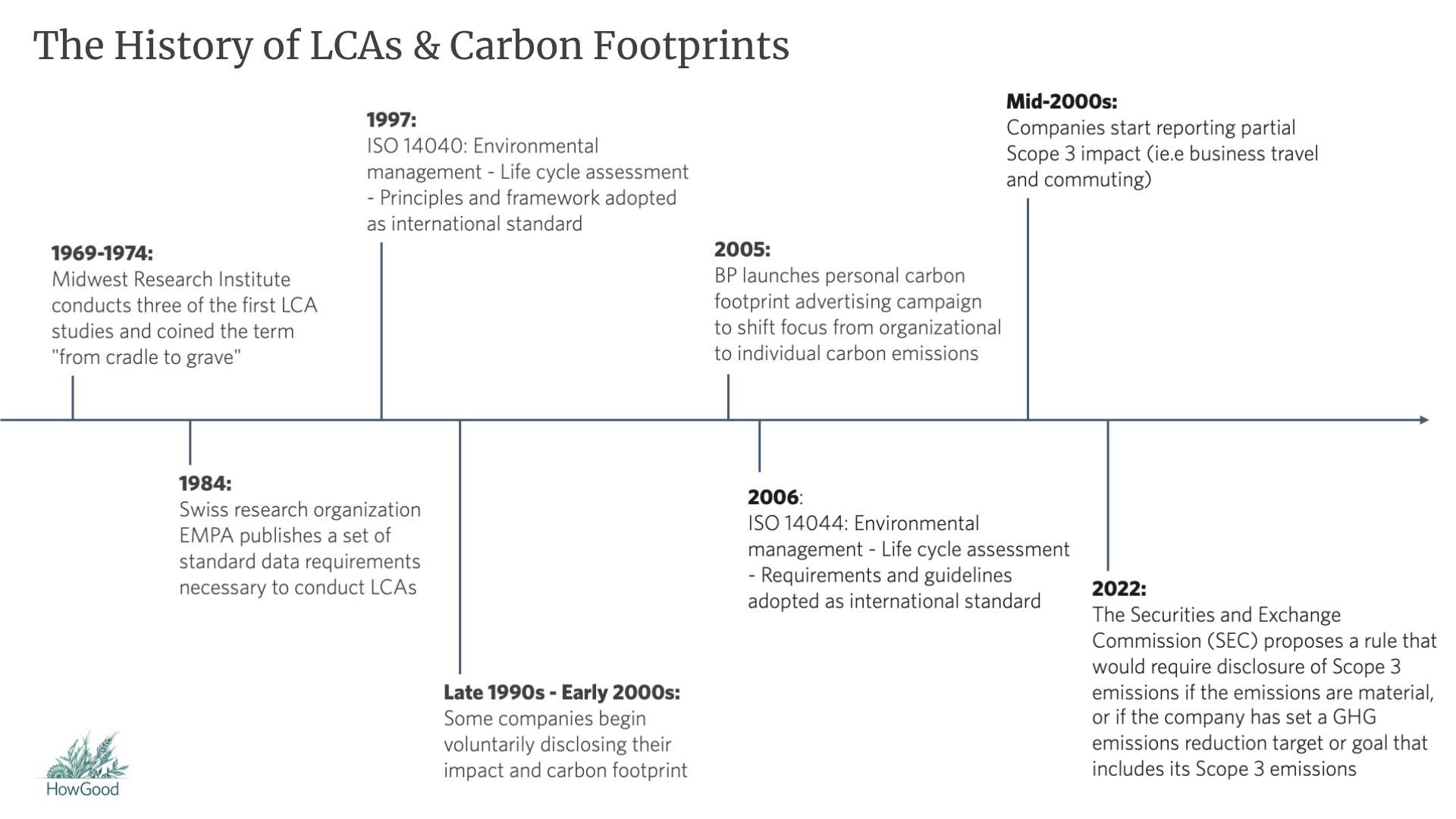

Thanks to an advertising campaign by fossil fuel giant BP in 2005, most consumers today are familiar with the concept of a personal carbon footprint. BP popularized the idea that individual action was the most effective method for reducing carbon being released into the atmosphere. This is, of course, untrue and seems like an especially egregious stance when taking into account that BP is responsible for nearly 26 million times more emissions than the average American annually.

It’s not solely fossil fuel companies that are to blame, though. Companies and organizations of all kinds are outsized contributors to climate change, much larger than any individual or household could ever be. Carbon footprinting came along as pressure mounted for companies to measure and report on their environmental impact and contribution to global warming.

It’s important to note that carbon footprinting for the purposes of GHG disclosure is completely voluntary from a regulatory standpoint. In the late 1990s and early 2000s, some companies chose to publicly disclose their impact, and while disclosure or reporting is voluntary, NGOs have developed frameworks on how to do so, which have evolved over time.

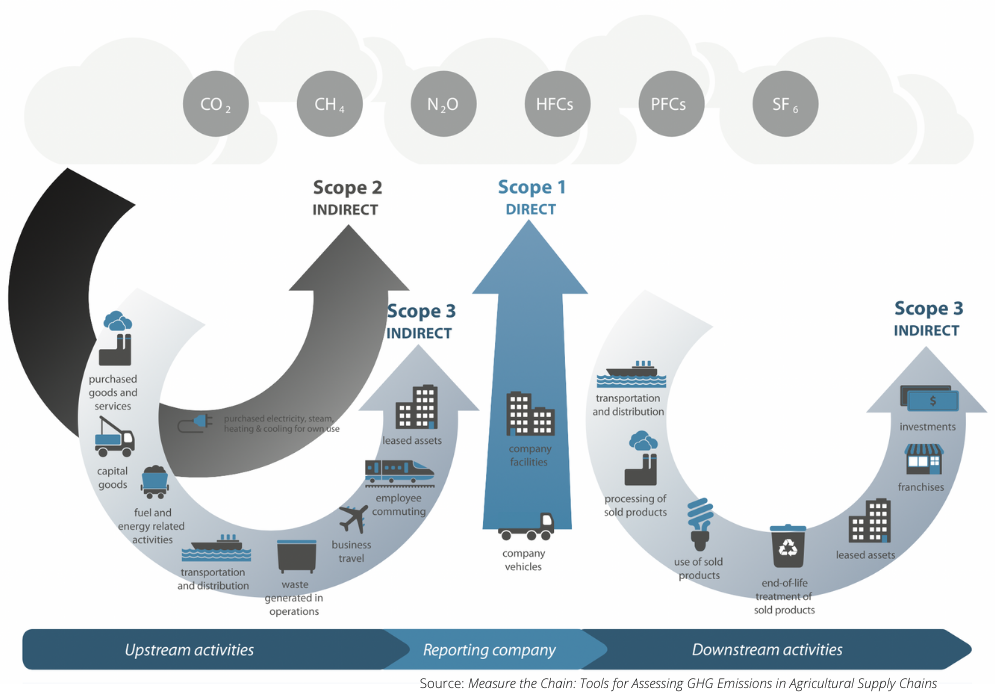

When it came to measuring Greenhouse Gas emissions (GHGe), Carbon Footprint Assessments were designed to measure and report on Scope 1 and 2 emissions, but not Scope 3. Scope 1 refers to direct emissions from sources a company owns or controls, Scope 2 refers to indirect emissions associated with purchased energy that is a part of a company’s operations, and Scope 3 refers to indirect emissions associated with sources not owned or controlled by a company. (See Figure 1)

Figure 1

Then, in the mid-2000s, companies started reporting (very) partial Scope 3 impact – business travel and sometimes commuting. These things are easy to estimate based on internal data that is relatively easily collectible via accounting and surveys, or through a travel vendor/app/credit card. As pressure has risen in recent years to include Scope 3 emissions in ESG reporting, a different measurement and reporting method – LCAs – rose to prominence.

History of LCAs

Scope 1-3 reporting using the GHG protocol is the most widely recognized method for assessing organizational and product greenhouse gas impact and is the standard to which HowGood adheres. One of the most prevalent tools within the protocol for assessing the scope 1, 2, and 3 impact of products, (and of materials going into products), is Life Cycle Assessment (LCA).

LCAs were originally born out of industrial ecology and were intended to compare products’ impacts. In the 1960s and 70s, LCAs had a fairly limited application evaluating whether ‘Product A’ had a smaller impact than ‘Product B’.

The current definition and use of the term Life Cycle Assessment rose to popularity in scientific literature in the early 2000s and was designed to evaluate the impact of a material or product from ‘cradle-to-grave’ including the use and disposal phases of a product. LCAs can either focus on carbon or measure multiple environmental and even social impacts such as water impact, indirect land use, and soil health.

LCAs were originally conceived for industrial settings; products like steel and aluminum which have discrete inputs and outputs allow for a more tactical application of these assessments. LCAs were not, however, designed with agricultural products in mind, and they tend to lag behind in this sphere.

The importance of carbon accounting in the food industry

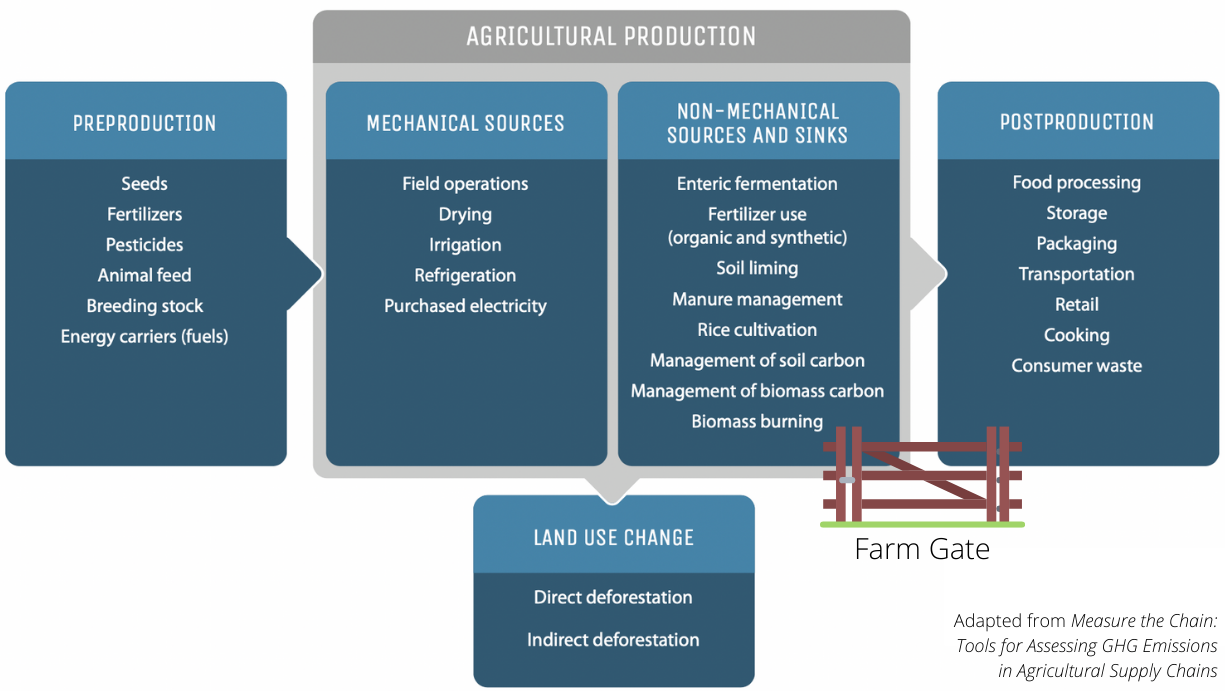

Carbon accounting is critical for the food industry in particular because the global food production system is responsible for more than a third of greenhouse gas emissions. For the majority of food products, 70-90% of their GHG impact occurs before the ingredients have even left the farm gate (see Figure 2). These qualify as Scope 3 emissions for food brands, CPGs, suppliers, and retailers:

Figure 2

While Scopes 1-2 are expected in the United States for ESG disclosures, a full reporting of Scope 3 emissions are increasingly expected by investors and NGOs because they are estimated to make up 50-70% percent of CPG companies’ total emissions. They are also the most challenging to report as the data lies largely outside of a company’s control.

Especially for a large organization that has hundreds or thousands of unique SKUs, doing full LCAs across an entire portfolio is not feasible from a cost, time, or qualified expert availability standpoint–particularly because assessments have to be done annually to meet reporting requirements.

Carbon Footprint Analysis can be viewed as one piece of a full life cycle assessment. Since LCAs include more than just GHG impact, they can offer a fuller picture of the environmental and social impacts of any given product.

For brands that are looking to tackle the GHG impact of their ingredients or products, perhaps as a first step in reducing overall environmental and social impact, carbon footprint analysis can be useful.

Weaknesses of Carbon Footprints

Although carbon emissions as a result of greenhouse gases and the burning of fossil fuels are the leading cause of climate change, (two of HowGood’s eight core sustainability metrics are related to GHG emissions), they are not the only indicators of environmental health. The need for more holistic methods of impact accounting is more evident than ever as the multitude of harmful effects of the global food system come into focus. Impacts such as biodiversity loss, freshwater use, land use, labor, and human rights risk, and resource depletion are not factored into carbon footprints.

If an organization is hoping to have a comprehensive look at an ingredient or group of ingredients, LCA may be best. That being said, although LCAs are more comprehensive in their scope, they do have limitations.

Weaknesses of Product LCAs

Static in nature

Perhaps the most conspicuous weakness of Life Cycle Assessments is their static nature. LCAs are a snapshot of a specific place where an ingredient is grown, at a specific time. This is an issue because the impact of any given ingredient varies greatly depending on geographical location.

For example, soy from Australia will have nearly 2 times the GHG impact of soy grown in the Midwestern United States due to hotter conditions and higher inputs needed for crop survival. Similarly, a tomato in the UK is likely grown in a greenhouse and will have a higher GHG impact than the same tomato grown in Spain that is cultivated outside and doesn’t require heat source inputs.

Additionally, as climate change causes the transfiguration of natural environments and the ecosystems where ingredients are grown, LCAs from even five or ten years ago have become outdated in their assessments of impact in that area.

Limited data

Product LCAs follow the four phases of a life cycle assessment:

- Goal and scope definition

- Inventory analysis

- Impact assessment

- Interpretation

Life cycle inventory (LCI) is a database of emissions factors used for the first three stages of the life cycle. The most popular inventories have more limited data than the studies available in the academic literature that HowGood draws from for quality, system boundaries, functional unit, and a host of other factors.

The types of gaps in data and the way they are filled affect the LCA greatly, and because there is no standardized method of doing so across different assessments, product LCAs are not comparable.

Assumptions and proxies

Due to the comprehensive nature of LCAs, and their objective of incorporating every factor and outcome of a production system, assumptions and estimates have to be made. It is rare to have a full data set to run an LCA, especially in agriculture, so proxies must be used to make assumptions to fill gaps in the data.

Many lifecycle resources have limited specificity for on-farm emissions and how they vary across crop-type and growing locations. To an industrial LCA consultant, apples and strawberries may seem to have more in common than disparities, but to an agricultural impact specialist, they are very obviously non-interchangeable.

Apples are a tree fruit that can be managed in a variety of systems and for 15-100+ years. Although strawberries are herbaceous biennials, they are largely managed as annual row crop systems that tend to be more dependent on tillage and reduced plant diversity.

Agricultural application

LCAs can have a particularly difficult time with agricultural fields because they are not engineered systems where complete control and measurement is possible. Agricultural systems are open and complex with much uncertainty.

Not to mention, some of the most updated reporting is ten years old, which is stale by many scientific literature standards but especially now when many ecosystems and agricultural growing locations have altered drastically due to climate change.

State of research & HowGood’s approach

The GHG Protocol’s Technical Guidance for Calculating Scope 3 Emissions outlines four methods of Scope 3 emissions reporting, requiring varying levels of commitment and resources for a CPG company to undertake.

HowGood’s goal is to incorporate intelligence into these methods in order to create a living LCA. One way that we do that is by using proxies differently from other organizations and consultants.

This means utilizing specific crop and location data, which allows for a more nimble and nuanced assessment–one that is not fixed in time and space. HowGood’s background in food, agricultural, environmental, and data systems allows for more precise use of proxies. (Meaning strawberries would not be considered interchangeable for apples when it comes to environmental impact.)

Carbon Life Cycle module

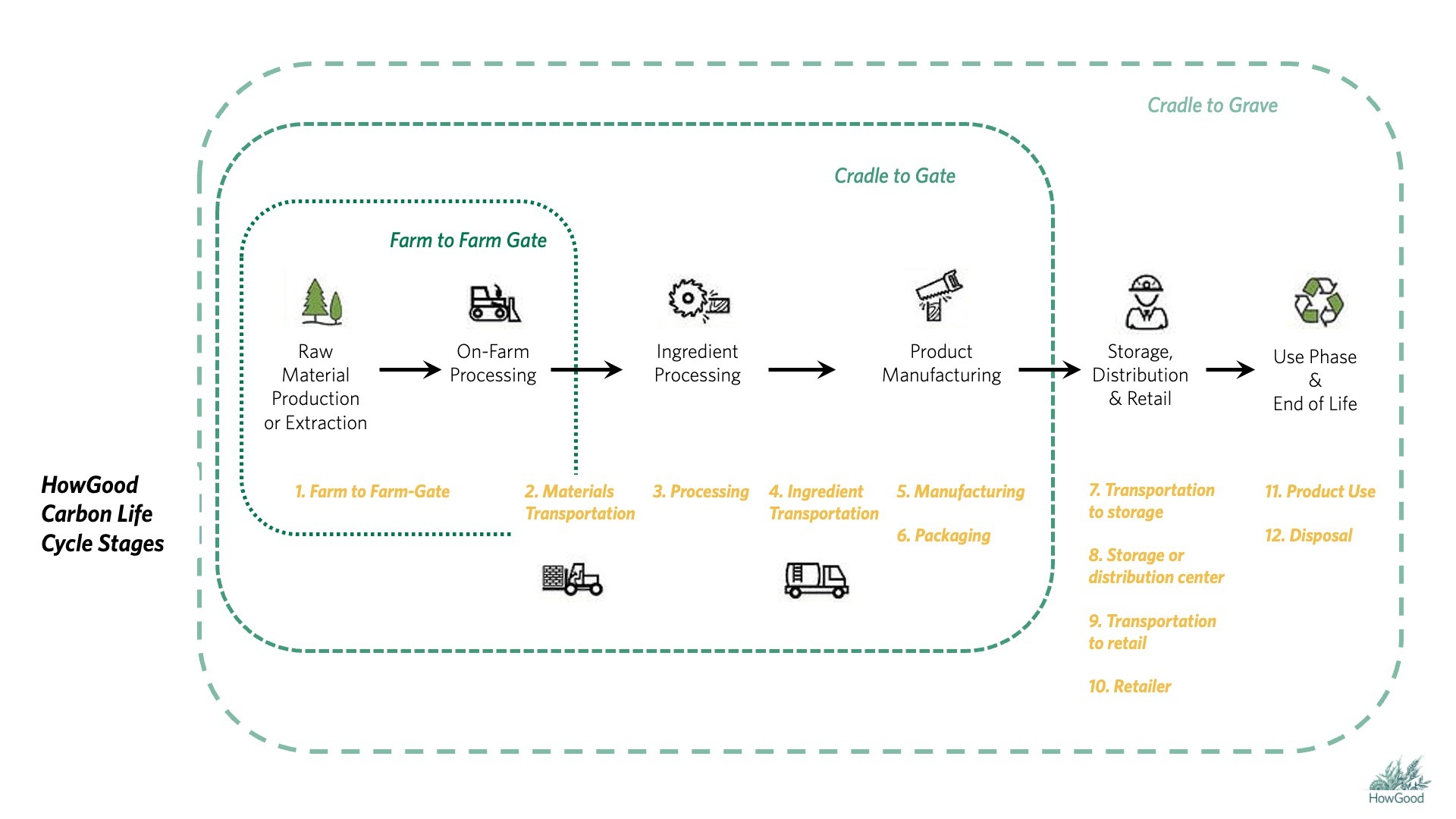

In addition to Latis, which measures sustainability impact holistically across a variety of metrics, HowGood’s Carbon Life Cycle module uses a unique approach to carbon accounting for food brands, CPGs, suppliers, and retailers. (See Figure 3) Firstly, its focus on Scope 3 emissions – specifically Field-to-Farm Gate emissions – allows companies to zero in on the part of their product supply system with the highest impact.

Figure 3

Perhaps most critically for larger brands, this method also makes it possible to execute carbon accounting and reporting at scale–something that would be nearly impossible by executing assessments on an individual ingredient or product basis.

The average data method which calculates cradle-to-gate emissions per unit of product is a viable method of reporting for companies who can pair basic product data with HowGood’s vast database of 33,000 ingredients, chemicals, and materials.

Conclusion

Deploying standardized tools like the HowGood Carbon Life Cycle module at scale could be the next evolution in carbon accounting. Regarding LCAs and more holistic approaches to impact accounting, using methods that incorporate the most up-to-date data and allow for geographic and temporal integration will be critical not only for the reduction of organizational environmental impact but also for meeting regulatory and consumer demands in the long term.

References:

- Guinée, J. B. (2011). Life cycle assessment: past, present, and future. Environmental Science & Technology, 45(1), 90-96. ACS Publications. 10.1021/es101316v

- Laurent, A., Olsen, S., & Hauschild, M. (2012). Limitations of Carbon Footprint as Indicator of Environmental Sustainability. Environmental Science and Tecnology, 46(7), 4100-4108. https://pubs.acs.org/doi/10.1021/es204163f

- LeBlanc, R. (2019, October 14). Comparing Carbon Footprint and Life Cycle Analyses. The Balance Small Business. Retrieved July 26, 2022, from https://www.thebalancesmb.com/carbon-footprint-vs-life-cycle-2878059

- World Resources Institute. (n.d.). Product Life Cycle Accounting and Reporting Standard. Greenhouse Gas Protocol |. Retrieved July 26, 2022, from https://ghgprotocol.org/sites/default/files/standards/Product-Life-Cycle-Accounting-Reporting-Standard_041613.pdf

More from the HowGood Blog:

- ‘Field to Farm Gate’: the Most Critical Piece of Scope 3 Emissions for Brands That Want to Reach Their ESG Goals

- Sourcing Ingredients with Smaller Carbon Footprints

- Food Eco-Labels: Re-Thinking Life Cycle Assessments

- The Time for Water-Thirsty Products is Over

- Identifying and Eliminating Labor Risk for a More Regenerative Global Food Supply

- An 8-Level Framework to Fight Biodiversity Loss